金融股在综合指数内占据重要的比重。

金融也也象征经济荣枯的迹象。

本季度最赚钱5大金融股的EPS在季度对比中都增长。

奇异的现象总在搜寻后发现。

你要仔细及用心的看。

KASSETS,领先一众产业股一匹马那么长。。。。。。

Alliance Research:

Below are our workings on Krissasset's fair value, after the announcement of its proposed IGB REIT listing. Based on the annualised 4Q11 core PBT and our back-of-the-envelope analysis, we have derived a fair value of RM8.95 per share, implying 27.7% upside from the last Friday closing price of RM7.01. We believe there is more upside than downside to our FV, given that there is high possibility of stronger earnings in FY12, which could result to higher value for its IGB REIT listing. In a nutshell, we see Krissasset as a no-brainer BUY (although we have no official coverage on the stock) and a safe heaven for FMs in the run up of 13th GE. After all, an annualised 55.3% return is a very good investment in any investment cycle!

KLCCP: Speculating that it is injecting its property portfolio into a REIT. REIT generally offer more attractive dividend yields, and are supported by a favorable tax structure. If it chooses to place its assets into a REIT, KLCCP could emerge as Malaysia’s largest REIT, with total assets worth rm12 billion. Its investment properties include Petronas Towers, Menera Maxis, Mandarin Oriental Hotel and Suria KLCC. It wholly owns Menara 3 Petronas, Menera Exxon Mobil and Komplexs Dayabumi.

KLCCP is up for re rating if it concurrently places its assets into a REIT and converts its RCULS. Upcoming earnings catalyst for KLCCP is a long term renewal for Menera Maxis in May 2013. KLCCP stands to get back rm1.2 billion cash or 96 sen per share fully diluted share if all its investment properties are injected into the REIT.

KLCCP is a 52.6% subsidiary of Petronas.

本季度最赚钱5大种植股:

有些的营业额增长,不过盈利跌。

有些EPS大跌,不过股价企稳。

当中是不是有奥妙的地方呢?

写在最后一张图上。

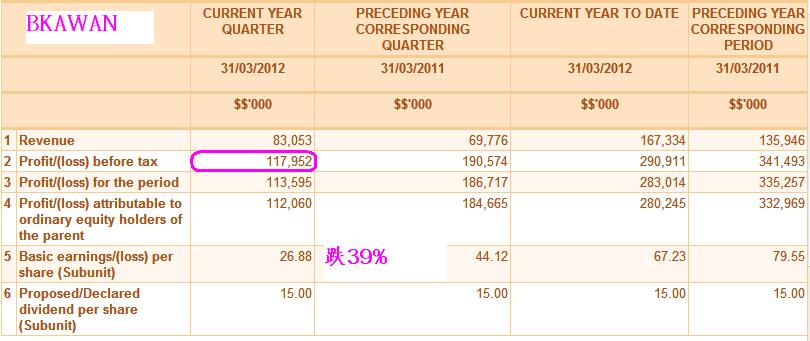

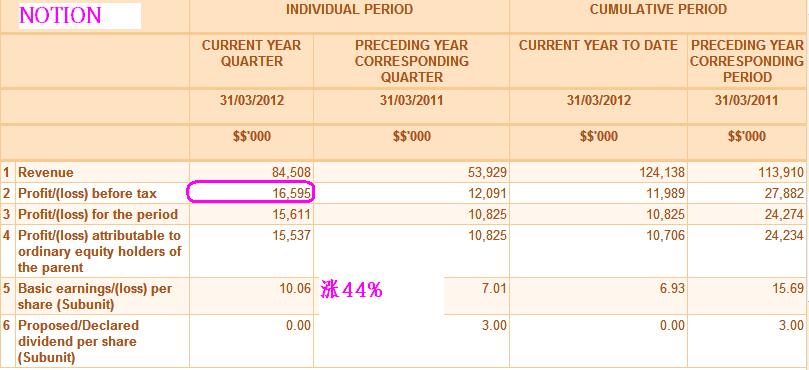

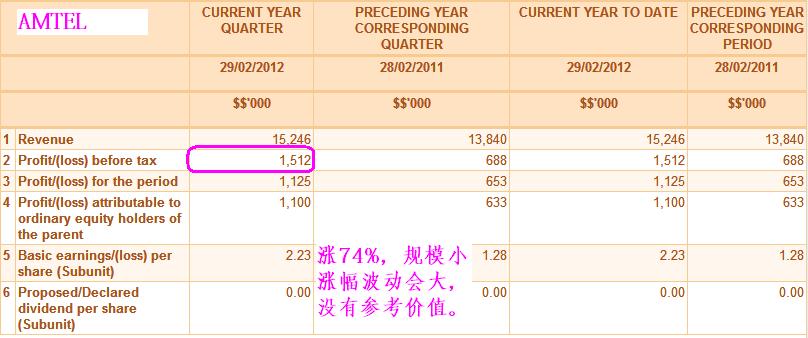

本季度最赚钱5大科技股:

{kind=link}

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.