1. 最近转让定价 [Transfer Pricing] 很红:

👉 你真的搞懂了吗?

👉 你真的学对了吗?

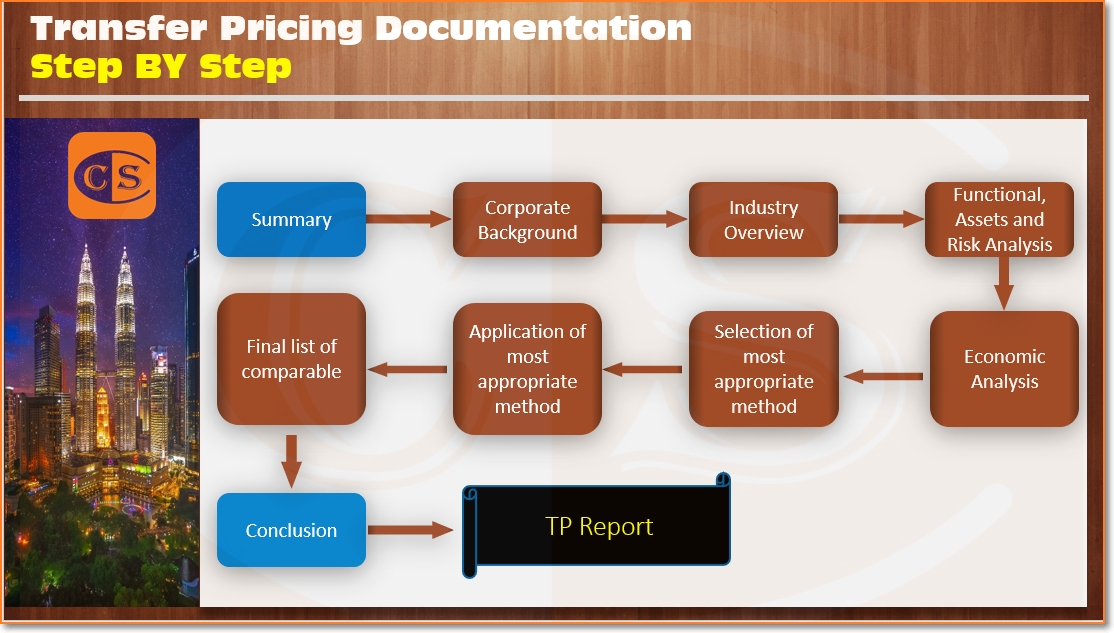

2. 如果想帮公司省点钱,也顺便想证明自己真的会 TP ,自己是否可以 DIY 准备一份 Limited TP Document?

3. 其实是可以的,只要你会。但是,你真的会吗?

4. 步骤也没有很多,但是要把这几个步骤做好,绝非一般的人做到的5. Do you want to be sure about your transfer pricing in Malaysia? Email to info@ccs-co.com

#TransferPricing

#转让定价系列

1. TP: 1 - 转让定价,究竟是骗术还是魔术

[A critique of Transfer Pricing: It's not art, science - its magic!]

👉 https://www.facebook.com/102267244519542/posts/449306889815574/

2. TP: 2.1 - 宜家家居玩转转让定价,绝世经典

[Ikea: flat pack tax avoidance through Transfer Pricing Arrangement]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-21-ikea-flat-pack-tax-avoidance.html

3. TP: 2.2 - 宜家家居玩转转让定价,2009年至2014年在欧盟避税估计10亿欧元

[IKEA transfer pricing strategy: disassembly instructions]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-22-2009201410-ikea-transfer-pricing.html

[A critique of Transfer Pricing: It's not art, science - its magic!]

👉 https://www.facebook.com/102267244519542/posts/449306889815574/

2. TP: 2.1 - 宜家家居玩转转让定价,绝世经典

[Ikea: flat pack tax avoidance through Transfer Pricing Arrangement]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-21-ikea-flat-pack-tax-avoidance.html

3. TP: 2.2 - 宜家家居玩转转让定价,2009年至2014年在欧盟避税估计10亿欧元

[IKEA transfer pricing strategy: disassembly instructions]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-22-2009201410-ikea-transfer-pricing.html

4. TP: 2.3 - IKEA 玩转转让定价,天衣无缝大师级的税筹 10亿欧元

[IKEA transfer pricing strategy: disassembly instructions]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-23-ikea-10-ikea-transfer-pricing.html

5. TP: 3 - 转让定价: 您需要知道的5件事

[5 things you should know about Transfer Pricing]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-3-5-5-things-you-should-know-about.html

[IKEA transfer pricing strategy: disassembly instructions]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-23-ikea-10-ikea-transfer-pricing.html

5. TP: 3 - 转让定价: 您需要知道的5件事

[5 things you should know about Transfer Pricing]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-3-5-5-things-you-should-know-about.html

6. TP: 4 - 转让定价: 税基侵蚀和利润转移的由来

[About BEPS, Base Erosion and Profit Shifting]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-4-about-beps-base-erosion-and-profit.html

[Selection of Methods (How, Why and Use of Methods)]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-5-selection-of-methods-how-why-and.html

8. TP: 6 - 谁需要准备转让定价文档

[Who should prepare Transfer Pricing Documentation]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-6-who-should-prepare-transfer.html

9. #Transfer Pricing 转让定价: 7 - 马来西亚的 “转让定价”

[Transfer Pricing In Malaysia]

👉 https://ccsyourauditor.blogspot.com/2021/01/tp-7-transfer-pricing-in-malaysia.html

10. #Transfer Pricing 转让定价: 8 - 关于”独立交易原则“,马来西亚有什么立法或法规?

[How Malaysia's legislation or regulation make reference to the Arm’s Length Principle?]

👉 https://ccsyourauditor.blogspot.com/2021/01/transfer-pricing-8-how-malaysias.html

11. #Transfer Pricing 转让定价: 9 - ”独立交易原则“的由来

[A brief History of the Arm’s Length Principle]

12. #Transfer Pricing 转让定价: 10 - OECD 转让定价指南在马来西亚所扮演的角色

[Role of the OECD Transfer Pricing Guidelines under Malaysia legislation]

👉 https://ccsyourauditor.blogspot.com/2021/01/transfer-pricing-10-oecd-role-of-oecd.html

13. #Transfer Pricing 转让定价: 11 - 马来西亚有任何法律或法规为“关联方”作出定义吗?

[Any Malaysia legislation or regulation provide a definition of related parties?]

14. #Transfer Pricing 转让定价: 12 - 马来西亚的转让定价方法

[Transfer Pricing Methods in Malaysia]

15. #Transfer Pricing 转让定价: 13 - 马来西亚"转让定价"方法的遴选准则

[Criterion uses in Malaysia for the application of transfer pricing methods]

👉 https://ccsyourauditor.blogspot.com/2021/01/transfer-pricing-13-criterion-uses-in.html

16. #Transfer Pricing 转让定价: 14 - 制药行业,如疫苗生产商行业特点及转让定价的问题

[Nature of the business/industry and market conditions of Pharmaceutical Industry]

https://ccsyourauditor.blogspot.com/2021/02/transfer-pricing-14-nature-of.html

☎️☎️☎️☎️☎️☎️☎️☎️☎️☎️☎️☎️

👉 专业资讯送到你手中

1. 本公司网站

✍️ https://www.ccs-co.com/

2. 本公司 Telegram

✍️ https://t.me/YourAuditor

【你需要先安装 Telegram】

3. 本公司 Instagram

✍ http://tiny.cc/rojzrz

4. 本公司部落格

✍ http://tiny.cc/8zjzrz

5. CCS Google

✍ http://tiny.cc/9oussz

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.