Individual investors who invest in equity crowdfunding platforms certified by the Securities Commission (SC) will be eligible for a tax exemption on a specified amount of aggregate income. This incentive was suggested in Budget 2021. The proposal has been legitimised by the Income Tax (Exemption) (No. 4) Order 2022.

投资于证券委员会(SC)认证的股权众筹平台的个人投资者的总收入将有资格获得特定金额的免税待遇。

这项税务优惠措施是在2021年预算案中被提出的。2022年所得税(豁免)(第4号)指使该建议立法。

Interpretation, For the purposes of the Exemption Order:

‘equity crowdfunding operator’ means:

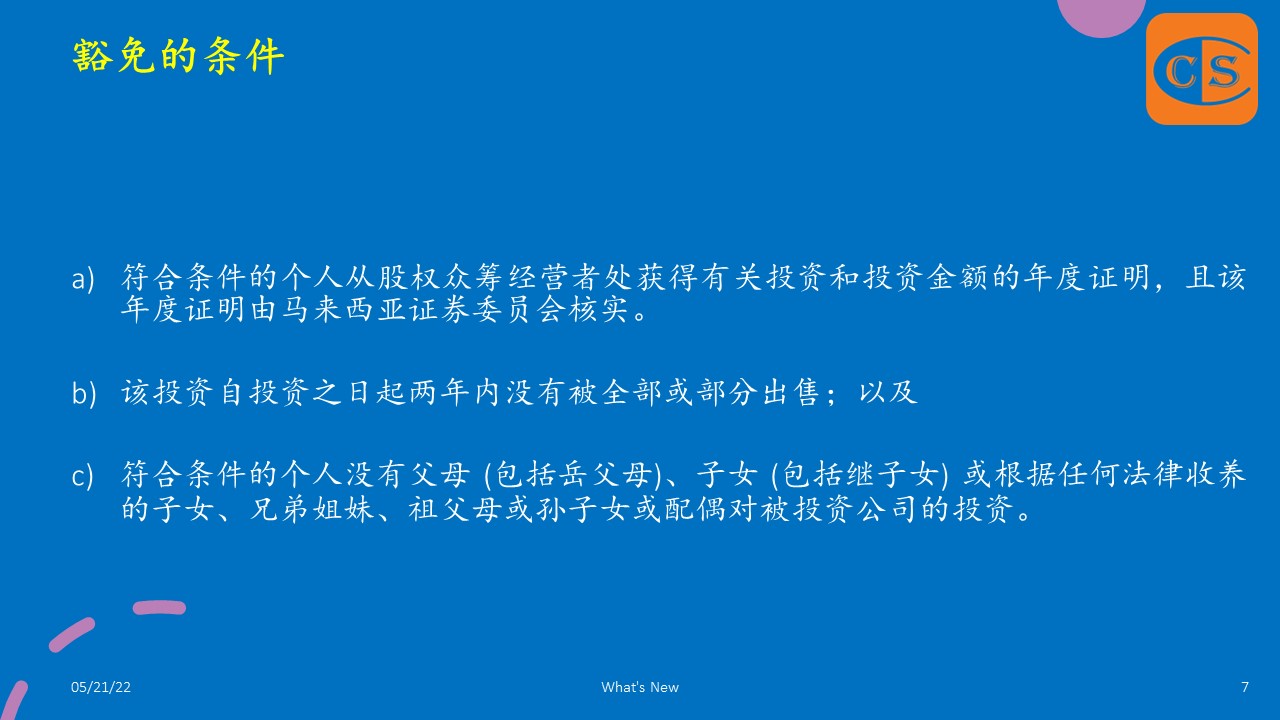

a) a company incorporated under the Companies Act 2016 (‘CA 2016’), and

b) registered with the SC as a recognised market operator to operate an equity crowdfunding platform under the SC’s Guidelines on Recognised Markets;

‘equity crowdfunding platform’

means an online equity fundraising platform operated by an equity crowdfunding operator;

‘Securities Commission Malaysia’

means the Securities Commission Malaysia established under section 3 of the SecuritiesCommissionMalaysiaAct1993 [Act 498];

‘nominee company’ means a company which is:

(a) incorporated under the CA 2016;

(b) resident in Malaysia; and

(c) established by an equity crowdfunding operator in Malaysia to receive investments from a qualifying individual for investment into an investee company through an equity crowdfunding platform;

‘investee company’ means a company that is:

(a) incorporated under the CA 2016, not including an exempt private company as specified in section 2 of the CA 2016;

(b) resident in Malaysia; and

(c) hosted on an equity crowdfunding platform to offer its shares;

‘shares’

means shares offered on the equity crowdfunding platform.

Non-application

The Exemption Order shall not apply to a qualifying individual:

who has made a claim for deduction under the Income Tax (Deduction for Investment in a Venture Company or Venture Capital Company Rules 2022 [P.U.(A)117/2022], or

who has been granted an exemption under the Income Tax (Exemption) Order (No. 3) 2014 [P.U.(A)167/2014].

解释

就此《豁免指令》而言:-

“股权众筹经营者”是指:

- 根据《2016年公司法令》("CA 2016")成立的公司;以及

- 根据证券委员会(SC) 的《认可市场准则》(Guidelines on Recognised Markets),向证券委员会(SC) 注册为认可市场经营者,以经营股权众筹平台。

“股权众筹平台”是指:

- 由股权众筹运营商运营的网络股权融资平台。

“马来西亚证券委员会” 是指:

- 根据《1993年马来西亚证券委员会法令》[第498号法] 第3条设立的马来西亚证券委员会。

“代名人公司” 是指:

- 根据《2016年公司法令》注册成立的公司;

- 马来西亚税务居民;以及

- 由股权众筹经营者在马来西亚设立的公司,以接受符合条件的个人投资者,通过股权众筹平台投资到被投资公司。

“被投资公司”是指:

- 根据《2016年公司法令》注册成立的公司,不包括《2016年公司法令》第2条规定的豁免私人公司;

- 马来西亚税务居民;以及

- 托管在股权众筹平台,以发售其股份。

“股份”是指:

- 股权众筹平台上发售的股份。

不适用

本豁免指令不适用于以下这些符合条件的个人:

- 根据《2022年所得税(投资于风险公司或风险投资公司的扣除)细则》[P.U.(A) 117/2022] 申请扣除的人,或

- 根据《2014年所得税(豁免)指令(第3号)》[P.U.(A) 167/2014] 获得豁免的人。

🌼🌼🌼🌼🌼🌼🌼🌼🌼🌼

Latest Updates #近期更新

1. The Publication of MIA’s Practice Review Annual Report 2020/2021

[MIA 2020/2021年 的实践审查年度报告]

https://lnkd.in/eRAErf68

2. Special Income Remittance Programme to Malaysian Residents

[源自外国汇入马来西亚的收入 特别报税方案]

🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳🌳

👉 Stay in touch with us

1. Website ✍️ https://www.ccs-co.com/

2. Telegram ✍️ http://bit.ly/YourAuditor

3. Instagram ✍ http://tiny.cc/rojzrz

4. Blog ✍ https://lnkd.in/e-Pu8_G

5. Google ✍ https://lnkd.in/ehZE6mxy

[MIA 2020/2021年 的实践审查年度报告]

https://lnkd.in/eRAErf68

2. Special Income Remittance Programme to Malaysian Residents

[源自外国汇入马来西亚的收入 特别报税方案]

https://lnkd.in/eqhVhXda

3. Post-implementation Review of IFRS 9 — Classification and Measurement

[国际财务报导准则第9号之 施行后检讨 —分类及衡量]

https://lnkd.in/eKCRJa-r

4. Adoption of ISQM 1, ISQM 2 and ISA 220 (Revised)

[ISQM 1、ISQM 2 和 ISA 220 (修订版)的采纳]

https://lnkd.in/eDbqMREV

5. Movable Property Security Interest (MPSI) Bill

[动产担保权益法案]

https://lnkd.in/esFqwA-u

6. IFRS Foundation announcement on the International Sustainability Standards Board (ISSB)

[国际财务报告准则基金会关于国际可持续发展 准则委员会的公告]

https://lnkd.in/e_2ZVynM

7. MASB Updates No.1 November 2021 - IFRS Interpretations Committee (IFRIC) Agenda Decisions

[马来西亚会计准则委员会 [MASB] 2021年11月第1号更新 - 国际财务报告准则解释委员会(IFRIC)议程决定]

https://lnkd.in/enJNxX9Q

8. MASB Updates No.1 November 2021 - IASB Project on Equity Method

[MASB 2021年11月第1号更新 - 会计准则理事会关于权益法 [Equity Method] 的项目]

https://lnkd.in/eu3ZX_rB

9. Bursa Malaysia issues updated Corporate Governance Guide

[马来西亚证券交易发布更新的 公司治理指南]

https://lnkd.in/e5pEbgpt

10. Amendments to the By-Laws (on professional ethics, conduct and practice) of MIA

[对 MIA 章程 (关于职业道德、行为和实践)的修订]

https://lnkd.in/euRvPuNy

11. Labuan Business Activity Tax (Requirements for Labuan Business Activity) Regulations 2021

[2021年纳闽商业活动税 (纳闽商业活动的要求)条例]

https://lnkd.in/etg252Kb

12. Pembangunan Sumber Manusia Berhad (Exemption of Levy) (No. 2) (Amendment) Order 2021 [2021 年人力资源发展有限公司 (免征征税)(第 2 号) (修订) 指令]

https://lnkd.in/eGmGXRaU

13. Income Tax (Exemption) (No. 11) Order 2021

[2021年所得税 (豁免)(第11号) 指令]

https://lnkd.in/e5e-J8SV

14. Income Tax (Exchange of Information) Rules 2021 - Request for Information

[2021年所得税 (信息交流) 细则 - 要求提供信息]

https://lnkd.in/eUCUWXK6

15. Stamp Duty (Exemption) (No. 11) 2021 (Amendment) Order 2021

[2021 年印花税(豁免) (第 11 号)(修订) 指令]

https://lnkd.in/e_NxSBxF

16. Income Tax (Exemption) (No. 13) 2013 (Amendment) Order 2021

[2021年所得税 (豁免)(第 13 号) 2013年(修订) 指令]

https://lnkd.in/ejJyjQFs

17. Income Tax Double Deduction for the Sponsorship of Scholarship to Malaysian Student

[赞助马来西亚学生奖学金的 所得税双重扣税]

https://lnkd.in/eZp57-Vi

18. Double Deduction for Expenditure on Provision of Employees’ Accommodation

[雇员住宿费用双重扣税]

https://lnkd.in/eWPN2Yrn

19. Starting from the YA 2022, Company Secretarial and Tax Filing Fees can claim Deduction even not PAID

[2022课税年度开始,公司秘书费及报税费用,没还钱也可以扣税了]

https://lnkd.in/eKfh7fkz

20. “MIA SMPs Channel” – a Dedicated Telegram Channel for SMPs

[中小会计事务所 (SMPs) 专用 Telegram 频道]

https://lnkd.in/eKR9nf5v

21. EPF: extension of 9% statutory contribution rate for Employees

[EPF: 延长雇员9% 的法定缴款率]

https://lnkd.in/eJsekn3Z

22. Income Tax (Industrial Building Allowance) (Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (工业建筑津贴)(敦拉萨国际贸易中心 Marquee 地位公司)(修订) 细则]

https://lnkd.in/eCiQHGP9

23. Income Tax (Accelerated Capital Allowance)(Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (资本津贴加速)(敦拉萨国际贸易中心Marquee 地位公司)(修订) 细则]

https://lnkd.in/eKNBf6vF

24. Income Tax (Deduction for Relocation Costs for Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (敦拉萨国际贸易中心 Marquee 地位公司 搬迁费用的扣除)(修订) 细则]

https://lnkd.in/e8UDx5Ki

25. Income Tax (Deduction for Rental Payments) (Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (租金扣除) (敦拉萨国际贸易中心 Marquee 地位公司)(修订) 细则]

https://lnkd.in/eiZAG8aP

26. Income Tax (Exemption) (No. 4) 2013 (Amendment) Order 2021

[2013年所得税 (豁免)(第4号) (修订) 指令]

https://lnkd.in/eH7V3YB3

27. Income Tax (Exemption) (No. 12) Order 2021

[2021年所得税 (豁免)(第12号) (修订) 指令]

https://lnkd.in/eyiVRAAr

28. Special Deduction for Reduction of Rental to SMEs extended to 30.6.2022

[中小型企业租金特别扣税延长至2022年6月]

https://lnkd.in/eFuafpPj

29. Special Deduction for Reduction of Rental to Non-SMEs Tenants extended to 30.6.2022

[非中小型企业租户租金特别扣税 延长至2022年6月]

https://lnkd.in/eiCFG9bS

30. Costs of Renovation and Refurbishment of Business Premise is allowable up to 31.12.2022

[营业场所翻修和翻新费用 扣税至2022年12月31日]

https://lnkd.in/dMe-u2bV

31. Tax Residents to be exempted from tax on the foreign-sourced income until Dec 31, 2026

[税务居民源自国外的收入将被免征税至2026年12月31日]

https://lnkd.in/eAu5rcJK

32. Export of Private Health Care Services – Tax Exemption

[出口私人保健服务 – 税务豁免]

https://lnkd.in/e9TrZnRQ

33. Instruments in relation to an approved M & A – Stamp Duty Exemption

[与批准的合并或收购有关的文件 – 豁免征收印花税]

https://lnkd.in/eS9EUKdv

34. Double Tax Deduction for the Sponsorship of Scholarship to Malaysian Student

[赞助马来西亚学生奖学金,所得税双重扣税]

https://lnkd.in/erNAhxAn

35. RM 20,000 Tax Rebate for the newly set up Company - ⚠️⚠️ Conditions apply ⚠️⚠️

[开新公司的2万令吉税务回扣是有条件的]

https://lnkd.in/e4HJG2AW

36. Finance Act 2021 has been Gazetted

[2021年财政法令已经在宪报颁布了]

https://lnkd.in/egpicBGF

37. IASB Exposure Draft ED/2021/9 Non-current Liabilities with Covenants (Proposed amendments to IAS 1)

[具合约条款之非流动负债 (国际会计准则第1号)]

https://lnkd.in/ehtBieY2

38. 38. IASB Exposure Draft ED/2021/10 Supplier Finance Arrangements (Proposed amendments to IAS 7 and IFRS 7)

[国际会计准则理事会征求意见稿ED/2021/10 供应商融资安排 (对国际会计准则7和国际财务报告准则7的拟议修正)]

https://lnkd.in/erky8JY2

39. SST – Guide on Food & Beverages

[服务税 - 食品和饮料指南]

https://lnkd.in/ehRuruRa

40. SST – Guide on Parking Services

[服务税 - 停车场服务指南]

https://lnkd.in/emFT9Ven

41. SST – Guide on Motor Vehicle Services or Repair

[服务税 - 机动车服务或维修指南]

https://lnkd.in/eU25Gkht

42. Double Tax Deduction for Expenditure in relation to Vendor Development Programme

[与供应商发展计划有关的支出双重扣税]

https://lnkd.in/ev2e4W8g

43. Tax Deduction for Investment in a Project of Commercialisation of Research and Development Findings

[研究与开发成果商业化项目投资 享有扣税资格]

https://lnkd.in/eZAfyv2S

44. FAQs on the implementation of Tax Identification Number, TIN

[这绝不是天上人间 而是TIN罗地网]

https://lnkd.in/eJvgtUpk

45. TP 1 表格,什么来的

[Something About “Form TP 1”]

https://lnkd.in/em-i-VWx

46. Statutory Minimum Wages - Why Pay Raise is Important?

[法定最低工资 – 为什么加薪很重要]

https://lnkd.in/eGEvjU6C

47. Accelerated Capital Allowance For Excursion Bus

[购买游览巴士享有加速资本津贴]

https://lnkd.in/eEEjDwvG

48. Deferment of the implementation of 2% Withholding Tax on Payment [Commission] Made To Agent etc.

[ 推迟执行向代理商、经销商、分销商支付佣金的2%预扣税]

https://lnkd.in/e-FkqG7b

49. HRD Levy Payment for the newly registered employers for January 2022 has been Resumed

[新注册的雇主,2022年1月恢复支付人力资源开发基金]

https://lnkd.in/e28NiHsv

50. Mandatory Adoption of Prescribed Forms CP21, CP22, CP22A, and CP22B

[强制性采用指定的表格 CP21、CP22、CP22A 和 CP22B]

https://lnkd.in/eBwiFntG

51. 只有在扣押令下 IRB 才有权要求银行提供你的信息

[Power to call for bank information for purpose of making a Garnishee Order application by IRB]

https://lnkd.in/eQsxcQV8

52. Tax Concessions Due to COVID-19 Travel Restrictions expired on 31 December 2021

[新冠肺炎期间的行动限制所给予的税务宽免于2021年12月31日结束]

https://lnkd.in/eqJzGEmN

53. Initial Application of MFRS 17 and MFRS 9 – Comparative Information (Amendment to MFRS 17 Insurance Contracts)

[初次应用 MFRS 17 和 MFRS 9 - 比较信息 (MFRS 17 保险合同的修正)]

https://lnkd.in/eUMMpfPQ

54. Filing Programme for Year 2022 - Employers

[2022年的申报安排 - 雇主 ]

https://lnkd.in/ee9mhwaW

55. Filing Programme for Year 2022 – Associations, Deceased Persons’ Estate and Hindu Joint Families

[2022年的申报安排 - 社团、死者遗产和印度教联合家庭]

https://lnkd.in/eFErzCmK

56. Filing Programme for Year 2022 – Other Individuals

[2022年的申报安排 - 其他人士]

https://lnkd.in/e3GgsDFg

57. Filing Programme for Year 2022 – Individuals, Partnerships

[2022年的申报安排 - 个人、合伙企业]

https://lnkd.in/ew8AdVYK

58. Filing Programme for Year 2022 – Trust Bodies and Co-Operative Societies

[2022年的申报安排 - 信托机构和合作社]

https://lnkd.in/eSG9P94S

59. Filing Programme for Year 2022 – Companies, Limited Liability Partnerships

[2022年的申报安排 - 公司、有限责任合伙公司]

https://lnkd.in/eQvAa6Dc

60. Filing Programme for Year 2022 – Real Estate Investment Trusts / Property Trust Funds, Business Trusts

[2022年的申报安排 - 房地产投资信托基金/财产信托基金,商业信托基金]

https://lnkd.in/ePzDNgcP

61. Guide Notes on Submission of Tax Returns

[关于提交纳税申报的指导说明]

https://lnkd.in/eekjaAzg

62. Minimum Wages (Amendment) Order 2022

[2022年最低工资(修正)指令]

https://lnkd.in/eYkYZEMR

63. All Accounting and Audit Firms having 10 or more employees are subject to HRD Levy

[所有聘请10人以上的会计和审计公司 都在人力资源发展征税范围内]

https://lnkd.in/evkTXh5G

64. MIA Qualifying Examination: Open for Registration Now

[MIA资格考试:开放注册! ]

https://lnkd.in/egegprJR

65. Incentive for Manufacturers of Pharmaceutical Products

[对医药产品制造商 的奖掖措施]

https://lnkd.in/eFB36Que

66. Withholding Tax on Payments Made to Agents, Dealers, and Distributors FAQ 1 - Overview

[于支付代理商、经销商和分销商款项预扣税的常见问题 - 概述]

https://lnkd.in/egtWUX79

67. 2% Withholding Tax on Payments Made to Agents, Dealers, and Distributors FAQ 2 - Meaning of Agents, Dealers, and Distributors

[于支付代理商、经销商和分销商款项预扣税的常见问题 - 代理商、经销商和分销商的含义]

https://lnkd.in/eTSmVJyn

68. Termination of Special Income Remittance Program

[最新消息 - 源自海外收入特别汇款计划]

https://lnkd.in/euW8CJzm

69. Financial Services (Minimum Amount of Capital Funds or Surplus of Assets over Liabilities) (Licensed Person) (Amendment) Order 2022

[2022年金融服务(资本金最低 限额或资产超过负债][持牌人] (修订)指令]

https://lnkd.in/eeyvXUxr

70. Islamic Financial Services (Minimum Amount of Capital Funds or Surplus of Assets over Liabilities) (Licensed Person) (Amendment) Order 2022

[2022年回教金融服务(资本金最低限额或资产超过负债][持牌人](修订)指令]

https://lnkd.in/ef-kcqih

71. Copyright (Amendment) Act 2022

[2022年 版权法(修正)法令]

https://lnkd.in/erESRUyR / https://lnkd.in/dAEvkVUh

72. Patents (Amendment) Act 2022

[2022年 专利法(修正)法令]

https://lnkd.in/dTV4i8wP / https://lnkd.in/d4xXqJV2

73. Geographical Indications Act 2022

[2022年 地理标志法令]

https://lnkd.in/dTV4i8wP / https://lnkd.in/d4xXqJV2

74. Tax Incentives for Sabah Development Corridor (SDC)

[沙巴发展走廊的 税收优惠措施 ]

https://lnkd.in/eFNHie7f / https://lnkd.in/ejH5wuzP

75. Tax Incentives for The East Coast Economic Region (ECER) - 1

[东海岸经济区(ECER) 的税收优惠政策 - 1]

https://lnkd.in/eZMu_hbr / https://lnkd.in/ewGqe6Zm

76. Tax Incentives for The East Coast Economic Region (ECER) - 2

[东海岸经济区(ECER) 的税收优惠政策 - 2]

https://lnkd.in/eCRrfdwX / https://lnkd.in/e7gsVj3w

77. Tax Incentives for The East Coast Economic Region (ECER) - 3

[东海岸经济区(ECER) 的税收优惠政策 - 3]

https://lnkd.in/eCRrfdwX / https://lnkd.in/e7gsVj3w

78. Tax Incentives for The East Coast Economic Region (ECER) - 4

[东海岸经济区(ECER) 的税收优惠政策 - 4]

https://lnkd.in/efTJ7fYw / https://lnkd.in/e6i3vF7c

79. Tax Incentives for The East Coast Economic Region (ECER) - 5

[东海岸经济区(ECER) 的税收优惠政策 - 5]

https://lnkd.in/ec-fjZJm / https://lnkd.in/eThw6gfP

80. 2022 edition of OECD Transfer Pricing Guidelines released

[2022年版 经合组织转让定价指南发布]

https://lnkd.in/eBWt7RiU / https://lnkd.in/eazntEkh

81. Partial Tax Exemption on Foreign Sourced Income in calculating Cukai Makmur

[计算繁荣税时,源自海外的收入享有部分豁免]

https://lnkd.in/ei8YCQVV / https://lnkd.in/eXPV-JGy

82. IRBM Revised 3 Tax Audit Frameworks

[税收局更新三个税务审计框架]

https://lnkd.in/eXcutqQK / https://lnkd.in/eFmNi5iu

83. Industrial Relations (Amendment) Regulations 2022

[2022年 劳资关系(修正)条例]

https://lnkd.in/eTFTpBbG / https://lnkd.in/e5c5bmPc

84. Income Tax (Exemption) (No. 2) Order 2022

[2022年所得税(豁免) (第2号)指令]

https://lnkd.in/e4n2_MPn / https://lnkd.in/eCizB2-Z

85. Income Tax (Exemption) (No. 3) Order 2022 - Venture Capital Management Company (VCMC) [2022年所得税(豁免) (第3号)指令 - 风险投资管理公司]

https://lnkd.in/eniBtSWg / https://lnkd.in/etvS27hy

86. Income Tax (Deduction for Investment in a Venture Company or Venture Capital Company) Rules 2022

[2022年所得税(对新创公司或 风险投资公司投资的扣除)细则]

https://lnkd.in/eSy4VXHR / https://lnkd.in/eaRieTCA

87. Strengthening Governance - Malaysian Code on Corporate Governance (MCCG) 2021

[加强治理 -- 2021年马来西亚公司治理准则 (MCCG)]

https://lnkd.in/e39TSZ-T / https://lnkd.in/eha2TDC7

3. Post-implementation Review of IFRS 9 — Classification and Measurement

[国际财务报导准则第9号之 施行后检讨 —分类及衡量]

https://lnkd.in/eKCRJa-r

4. Adoption of ISQM 1, ISQM 2 and ISA 220 (Revised)

[ISQM 1、ISQM 2 和 ISA 220 (修订版)的采纳]

https://lnkd.in/eDbqMREV

5. Movable Property Security Interest (MPSI) Bill

[动产担保权益法案]

https://lnkd.in/esFqwA-u

6. IFRS Foundation announcement on the International Sustainability Standards Board (ISSB)

[国际财务报告准则基金会关于国际可持续发展 准则委员会的公告]

https://lnkd.in/e_2ZVynM

7. MASB Updates No.1 November 2021 - IFRS Interpretations Committee (IFRIC) Agenda Decisions

[马来西亚会计准则委员会 [MASB] 2021年11月第1号更新 - 国际财务报告准则解释委员会(IFRIC)议程决定]

https://lnkd.in/enJNxX9Q

8. MASB Updates No.1 November 2021 - IASB Project on Equity Method

[MASB 2021年11月第1号更新 - 会计准则理事会关于权益法 [Equity Method] 的项目]

https://lnkd.in/eu3ZX_rB

9. Bursa Malaysia issues updated Corporate Governance Guide

[马来西亚证券交易发布更新的 公司治理指南]

https://lnkd.in/e5pEbgpt

10. Amendments to the By-Laws (on professional ethics, conduct and practice) of MIA

[对 MIA 章程 (关于职业道德、行为和实践)的修订]

https://lnkd.in/euRvPuNy

11. Labuan Business Activity Tax (Requirements for Labuan Business Activity) Regulations 2021

[2021年纳闽商业活动税 (纳闽商业活动的要求)条例]

https://lnkd.in/etg252Kb

12. Pembangunan Sumber Manusia Berhad (Exemption of Levy) (No. 2) (Amendment) Order 2021 [2021 年人力资源发展有限公司 (免征征税)(第 2 号) (修订) 指令]

https://lnkd.in/eGmGXRaU

13. Income Tax (Exemption) (No. 11) Order 2021

[2021年所得税 (豁免)(第11号) 指令]

https://lnkd.in/e5e-J8SV

14. Income Tax (Exchange of Information) Rules 2021 - Request for Information

[2021年所得税 (信息交流) 细则 - 要求提供信息]

https://lnkd.in/eUCUWXK6

15. Stamp Duty (Exemption) (No. 11) 2021 (Amendment) Order 2021

[2021 年印花税(豁免) (第 11 号)(修订) 指令]

https://lnkd.in/e_NxSBxF

16. Income Tax (Exemption) (No. 13) 2013 (Amendment) Order 2021

[2021年所得税 (豁免)(第 13 号) 2013年(修订) 指令]

https://lnkd.in/ejJyjQFs

17. Income Tax Double Deduction for the Sponsorship of Scholarship to Malaysian Student

[赞助马来西亚学生奖学金的 所得税双重扣税]

https://lnkd.in/eZp57-Vi

18. Double Deduction for Expenditure on Provision of Employees’ Accommodation

[雇员住宿费用双重扣税]

https://lnkd.in/eWPN2Yrn

19. Starting from the YA 2022, Company Secretarial and Tax Filing Fees can claim Deduction even not PAID

[2022课税年度开始,公司秘书费及报税费用,没还钱也可以扣税了]

https://lnkd.in/eKfh7fkz

20. “MIA SMPs Channel” – a Dedicated Telegram Channel for SMPs

[中小会计事务所 (SMPs) 专用 Telegram 频道]

https://lnkd.in/eKR9nf5v

21. EPF: extension of 9% statutory contribution rate for Employees

[EPF: 延长雇员9% 的法定缴款率]

https://lnkd.in/eJsekn3Z

22. Income Tax (Industrial Building Allowance) (Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (工业建筑津贴)(敦拉萨国际贸易中心 Marquee 地位公司)(修订) 细则]

https://lnkd.in/eCiQHGP9

23. Income Tax (Accelerated Capital Allowance)(Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (资本津贴加速)(敦拉萨国际贸易中心Marquee 地位公司)(修订) 细则]

https://lnkd.in/eKNBf6vF

24. Income Tax (Deduction for Relocation Costs for Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (敦拉萨国际贸易中心 Marquee 地位公司 搬迁费用的扣除)(修订) 细则]

https://lnkd.in/e8UDx5Ki

25. Income Tax (Deduction for Rental Payments) (Tun Razak Exchange Marquee Status Company) (Amendment) Rules 2021

[2021年所得税 (租金扣除) (敦拉萨国际贸易中心 Marquee 地位公司)(修订) 细则]

https://lnkd.in/eiZAG8aP

26. Income Tax (Exemption) (No. 4) 2013 (Amendment) Order 2021

[2013年所得税 (豁免)(第4号) (修订) 指令]

https://lnkd.in/eH7V3YB3

27. Income Tax (Exemption) (No. 12) Order 2021

[2021年所得税 (豁免)(第12号) (修订) 指令]

https://lnkd.in/eyiVRAAr

28. Special Deduction for Reduction of Rental to SMEs extended to 30.6.2022

[中小型企业租金特别扣税延长至2022年6月]

https://lnkd.in/eFuafpPj

29. Special Deduction for Reduction of Rental to Non-SMEs Tenants extended to 30.6.2022

[非中小型企业租户租金特别扣税 延长至2022年6月]

https://lnkd.in/eiCFG9bS

30. Costs of Renovation and Refurbishment of Business Premise is allowable up to 31.12.2022

[营业场所翻修和翻新费用 扣税至2022年12月31日]

https://lnkd.in/dMe-u2bV

31. Tax Residents to be exempted from tax on the foreign-sourced income until Dec 31, 2026

[税务居民源自国外的收入将被免征税至2026年12月31日]

https://lnkd.in/eAu5rcJK

32. Export of Private Health Care Services – Tax Exemption

[出口私人保健服务 – 税务豁免]

https://lnkd.in/e9TrZnRQ

33. Instruments in relation to an approved M & A – Stamp Duty Exemption

[与批准的合并或收购有关的文件 – 豁免征收印花税]

https://lnkd.in/eS9EUKdv

34. Double Tax Deduction for the Sponsorship of Scholarship to Malaysian Student

[赞助马来西亚学生奖学金,所得税双重扣税]

https://lnkd.in/erNAhxAn

35. RM 20,000 Tax Rebate for the newly set up Company - ⚠️⚠️ Conditions apply ⚠️⚠️

[开新公司的2万令吉税务回扣是有条件的]

https://lnkd.in/e4HJG2AW

36. Finance Act 2021 has been Gazetted

[2021年财政法令已经在宪报颁布了]

https://lnkd.in/egpicBGF

37. IASB Exposure Draft ED/2021/9 Non-current Liabilities with Covenants (Proposed amendments to IAS 1)

[具合约条款之非流动负债 (国际会计准则第1号)]

https://lnkd.in/ehtBieY2

38. 38. IASB Exposure Draft ED/2021/10 Supplier Finance Arrangements (Proposed amendments to IAS 7 and IFRS 7)

[国际会计准则理事会征求意见稿ED/2021/10 供应商融资安排 (对国际会计准则7和国际财务报告准则7的拟议修正)]

https://lnkd.in/erky8JY2

39. SST – Guide on Food & Beverages

[服务税 - 食品和饮料指南]

https://lnkd.in/ehRuruRa

40. SST – Guide on Parking Services

[服务税 - 停车场服务指南]

https://lnkd.in/emFT9Ven

41. SST – Guide on Motor Vehicle Services or Repair

[服务税 - 机动车服务或维修指南]

https://lnkd.in/eU25Gkht

42. Double Tax Deduction for Expenditure in relation to Vendor Development Programme

[与供应商发展计划有关的支出双重扣税]

https://lnkd.in/ev2e4W8g

43. Tax Deduction for Investment in a Project of Commercialisation of Research and Development Findings

[研究与开发成果商业化项目投资 享有扣税资格]

https://lnkd.in/eZAfyv2S

44. FAQs on the implementation of Tax Identification Number, TIN

[这绝不是天上人间 而是TIN罗地网]

https://lnkd.in/eJvgtUpk

45. TP 1 表格,什么来的

[Something About “Form TP 1”]

https://lnkd.in/em-i-VWx

46. Statutory Minimum Wages - Why Pay Raise is Important?

[法定最低工资 – 为什么加薪很重要]

https://lnkd.in/eGEvjU6C

47. Accelerated Capital Allowance For Excursion Bus

[购买游览巴士享有加速资本津贴]

https://lnkd.in/eEEjDwvG

48. Deferment of the implementation of 2% Withholding Tax on Payment [Commission] Made To Agent etc.

[ 推迟执行向代理商、经销商、分销商支付佣金的2%预扣税]

https://lnkd.in/e-FkqG7b

49. HRD Levy Payment for the newly registered employers for January 2022 has been Resumed

[新注册的雇主,2022年1月恢复支付人力资源开发基金]

https://lnkd.in/e28NiHsv

50. Mandatory Adoption of Prescribed Forms CP21, CP22, CP22A, and CP22B

[强制性采用指定的表格 CP21、CP22、CP22A 和 CP22B]

https://lnkd.in/eBwiFntG

51. 只有在扣押令下 IRB 才有权要求银行提供你的信息

[Power to call for bank information for purpose of making a Garnishee Order application by IRB]

https://lnkd.in/eQsxcQV8

52. Tax Concessions Due to COVID-19 Travel Restrictions expired on 31 December 2021

[新冠肺炎期间的行动限制所给予的税务宽免于2021年12月31日结束]

https://lnkd.in/eqJzGEmN

53. Initial Application of MFRS 17 and MFRS 9 – Comparative Information (Amendment to MFRS 17 Insurance Contracts)

[初次应用 MFRS 17 和 MFRS 9 - 比较信息 (MFRS 17 保险合同的修正)]

https://lnkd.in/eUMMpfPQ

54. Filing Programme for Year 2022 - Employers

[2022年的申报安排 - 雇主 ]

https://lnkd.in/ee9mhwaW

55. Filing Programme for Year 2022 – Associations, Deceased Persons’ Estate and Hindu Joint Families

[2022年的申报安排 - 社团、死者遗产和印度教联合家庭]

https://lnkd.in/eFErzCmK

56. Filing Programme for Year 2022 – Other Individuals

[2022年的申报安排 - 其他人士]

https://lnkd.in/e3GgsDFg

57. Filing Programme for Year 2022 – Individuals, Partnerships

[2022年的申报安排 - 个人、合伙企业]

https://lnkd.in/ew8AdVYK

58. Filing Programme for Year 2022 – Trust Bodies and Co-Operative Societies

[2022年的申报安排 - 信托机构和合作社]

https://lnkd.in/eSG9P94S

59. Filing Programme for Year 2022 – Companies, Limited Liability Partnerships

[2022年的申报安排 - 公司、有限责任合伙公司]

https://lnkd.in/eQvAa6Dc

60. Filing Programme for Year 2022 – Real Estate Investment Trusts / Property Trust Funds, Business Trusts

[2022年的申报安排 - 房地产投资信托基金/财产信托基金,商业信托基金]

https://lnkd.in/ePzDNgcP

61. Guide Notes on Submission of Tax Returns

[关于提交纳税申报的指导说明]

https://lnkd.in/eekjaAzg

62. Minimum Wages (Amendment) Order 2022

[2022年最低工资(修正)指令]

https://lnkd.in/eYkYZEMR

63. All Accounting and Audit Firms having 10 or more employees are subject to HRD Levy

[所有聘请10人以上的会计和审计公司 都在人力资源发展征税范围内]

https://lnkd.in/evkTXh5G

64. MIA Qualifying Examination: Open for Registration Now

[MIA资格考试:开放注册! ]

https://lnkd.in/egegprJR

65. Incentive for Manufacturers of Pharmaceutical Products

[对医药产品制造商 的奖掖措施]

https://lnkd.in/eFB36Que

66. Withholding Tax on Payments Made to Agents, Dealers, and Distributors FAQ 1 - Overview

[于支付代理商、经销商和分销商款项预扣税的常见问题 - 概述]

https://lnkd.in/egtWUX79

67. 2% Withholding Tax on Payments Made to Agents, Dealers, and Distributors FAQ 2 - Meaning of Agents, Dealers, and Distributors

[于支付代理商、经销商和分销商款项预扣税的常见问题 - 代理商、经销商和分销商的含义]

https://lnkd.in/eTSmVJyn

68. Termination of Special Income Remittance Program

[最新消息 - 源自海外收入特别汇款计划]

https://lnkd.in/euW8CJzm

69. Financial Services (Minimum Amount of Capital Funds or Surplus of Assets over Liabilities) (Licensed Person) (Amendment) Order 2022

[2022年金融服务(资本金最低 限额或资产超过负债][持牌人] (修订)指令]

https://lnkd.in/eeyvXUxr

70. Islamic Financial Services (Minimum Amount of Capital Funds or Surplus of Assets over Liabilities) (Licensed Person) (Amendment) Order 2022

[2022年回教金融服务(资本金最低限额或资产超过负债][持牌人](修订)指令]

https://lnkd.in/ef-kcqih

71. Copyright (Amendment) Act 2022

[2022年 版权法(修正)法令]

https://lnkd.in/erESRUyR / https://lnkd.in/dAEvkVUh

72. Patents (Amendment) Act 2022

[2022年 专利法(修正)法令]

https://lnkd.in/dTV4i8wP / https://lnkd.in/d4xXqJV2

73. Geographical Indications Act 2022

[2022年 地理标志法令]

https://lnkd.in/dTV4i8wP / https://lnkd.in/d4xXqJV2

74. Tax Incentives for Sabah Development Corridor (SDC)

[沙巴发展走廊的 税收优惠措施 ]

https://lnkd.in/eFNHie7f / https://lnkd.in/ejH5wuzP

75. Tax Incentives for The East Coast Economic Region (ECER) - 1

[东海岸经济区(ECER) 的税收优惠政策 - 1]

https://lnkd.in/eZMu_hbr / https://lnkd.in/ewGqe6Zm

76. Tax Incentives for The East Coast Economic Region (ECER) - 2

[东海岸经济区(ECER) 的税收优惠政策 - 2]

https://lnkd.in/eCRrfdwX / https://lnkd.in/e7gsVj3w

77. Tax Incentives for The East Coast Economic Region (ECER) - 3

[东海岸经济区(ECER) 的税收优惠政策 - 3]

https://lnkd.in/eCRrfdwX / https://lnkd.in/e7gsVj3w

78. Tax Incentives for The East Coast Economic Region (ECER) - 4

[东海岸经济区(ECER) 的税收优惠政策 - 4]

https://lnkd.in/efTJ7fYw / https://lnkd.in/e6i3vF7c

79. Tax Incentives for The East Coast Economic Region (ECER) - 5

[东海岸经济区(ECER) 的税收优惠政策 - 5]

https://lnkd.in/ec-fjZJm / https://lnkd.in/eThw6gfP

80. 2022 edition of OECD Transfer Pricing Guidelines released

[2022年版 经合组织转让定价指南发布]

https://lnkd.in/eBWt7RiU / https://lnkd.in/eazntEkh

81. Partial Tax Exemption on Foreign Sourced Income in calculating Cukai Makmur

[计算繁荣税时,源自海外的收入享有部分豁免]

https://lnkd.in/ei8YCQVV / https://lnkd.in/eXPV-JGy

82. IRBM Revised 3 Tax Audit Frameworks

[税收局更新三个税务审计框架]

https://lnkd.in/eXcutqQK / https://lnkd.in/eFmNi5iu

83. Industrial Relations (Amendment) Regulations 2022

[2022年 劳资关系(修正)条例]

https://lnkd.in/eTFTpBbG / https://lnkd.in/e5c5bmPc

84. Income Tax (Exemption) (No. 2) Order 2022

[2022年所得税(豁免) (第2号)指令]

https://lnkd.in/e4n2_MPn / https://lnkd.in/eCizB2-Z

85. Income Tax (Exemption) (No. 3) Order 2022 - Venture Capital Management Company (VCMC) [2022年所得税(豁免) (第3号)指令 - 风险投资管理公司]

https://lnkd.in/eniBtSWg / https://lnkd.in/etvS27hy

86. Income Tax (Deduction for Investment in a Venture Company or Venture Capital Company) Rules 2022

[2022年所得税(对新创公司或 风险投资公司投资的扣除)细则]

https://lnkd.in/eSy4VXHR / https://lnkd.in/eaRieTCA

87. Strengthening Governance - Malaysian Code on Corporate Governance (MCCG) 2021

[加强治理 -- 2021年马来西亚公司治理准则 (MCCG)]

https://lnkd.in/e39TSZ-T / https://lnkd.in/eha2TDC7

88. Malaysian Code on Corporate Governance (MCCG) 2021 - Key Updates

[2021年 马来西亚公司治理准则 - 关键的更新]

89. Responses from the LHDN to CTIM Comments - FAQ on 2% Withholding Tax Deducted from Payment by Payer Companies to Agents, Dealers, and Distributors

[LHDN 对CTIM 意见的回应 -- 关于付款人公司向代理商、经销商和分销商支付的款项中扣除2%预扣税的常见问题]

90. Service Tax Policy No. 3/2021 - Service Tax Exemption on Brokerage Services

[第3/2021号服务税政策 - 经纪服务的服务税豁免]

91. Indirect Tax Special Voluntary Disclosure & Amnesty Program - Guideline & FAQs

[间接税 特别自愿披露和赦免计划 - 指南与常见问题]

92. Tourism Tax (TTx) Policy No. 2/2021 - Extension of TTx Exemption

[第2/2021号 旅游税(TTx)政策 - 延长旅游税豁免期]

93. Revised Guide on Advertising Services dated 19 January 2022

[2022年1月19日的《广告服务指南》修订版]

94. Approved Major Exporter Scheme (AMES) - Updated news

[核准的主要出口商计划 - 最新新闻]

95. Service Tax Policy No. 3/2021 (Amendment No. 1) - Service Tax Exemption for Brokerage Services

[第3/2021号服务税政策(第1号修正案) – 免除经纪服务的服务税]

96. Sales Tax Policy No. 1/2022 - Sales Tax Exemption on Pallets

[第1/2022号 销售税政策 - 托盘的销售税豁免]

97. IESBA: Objectivity of Engagement Quality Reviewer and Other Appropriate Reviewers

[IESBA 发布指引强调 – 相关复核人员遵循客观公正原则的重要性]

98. Employment (Amendment) Act 2022

👉 Stay in touch with us

1. Website ✍️ https://www.ccs-co.com/

2. Telegram ✍️ http://bit.ly/YourAuditor

3. Instagram ✍ http://tiny.cc/rojzrz

4. Blog ✍ https://lnkd.in/e-Pu8_G

5. Google ✍ https://lnkd.in/ehZE6mxy

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.